Content

As with many other metrics, this model depends on the industry and the final product. For each business model, the conversion funnel looks different.

What type of cost is conversion cost?

Conversion costs are expenses for overhead and direct labor related to the conversion of raw materials into products. Conversion costs are similar to prime costs, except that the latter consists of costs related to direct labor and direct materials, not direct labor and overhead.

Therefore, the conversion cost per unit for the month was $6.80 per unit (calculated as $136,000 of total conversion costs divided by the 20,000 units produced). Conversion costs include all direct or indirect production costs incurred in activities that convert raw materials into finished products. Let’s assume that the organization has produced 2,500 units of a product in the first quarter of FY2020. The manufacturing overheads of the production include the depreciation of $5,000, insurance costs of $10,000, maintenance costs of $5,000 and electricity costs of $10,000. Direct materials and direct labor charges are both included in prime costs when creating full items. The acquisition of raw materials or any physical element required to produce a product is referred to as direct materials. Hence, using conversion costs is an efficient way of calculating equivalent units and per unit cost rather than separately calculating direct labor and manufacturing overheads.

Prime Costs vs. Conversion Costs

You’d also want to avoid incurring unnecessary costs, and knowing which costs are necessary for the conversion of your raw materials will help you with that. A targeted campaign is sure to increase your conversion rate. And better conversion rate helps you reduce the conversion cost.

- In production/ manufacturing as it considers only two elements – direct labour and overheads.

- Prime costs are defined as the expenditures directly related to creating finished products, while conversion costs are the expenses incurred when turning raw materials into a product.

- Direct labor is counted as both a prime cost and a conversion cost.

Conversion costs are also used as a measure to gauge the efficiencies in production processes but take into account the overhead expenses left out of prime cost calculations. Operations managers also use conversion costs to determine where there may be waste within the manufacturing process. Calculating equivalent units and unit costs by adding direct labor and manufacturing overheads is more time-saving than calculating the two costs separately. The prime cost of making this bed will include direct labor and raw materials.

Accounting Topics

The prime costs for creating the table include both the cost of the furniture maker’s labor and the raw materials required to construct the table, including the lumber, hardware, and paint. Prime CostPrime cost is the direct cost incurred in manufacturing a product and typically includes the direct production cost of goods, raw material and direct labour costs. Costing and effective pricing of the goods are primarily determined on their basis. Prime cost is the direct cost incurred in manufacturing a product and typically includes the direct production cost of goods, raw material and direct labour costs. Then total direct labor costs and total manufacturing overhead are added. The conversion cost is calculated to estimate production expenses, develop product pricing models, and estimate the value of finished product inventory. Managers also use this cost to evaluate the efficiency of the production process.

- The main goal of prime costs is to help financial and operation managers set product prices, which will result in a significant profit.

- Meanwhile, increase your bids for campaigns with lower conversion costs.

- The costs of the employees who make the goods are known as direct labor expenses.

- Inventory-producing companies rely significantly on specific indicators to measure production and assess how efficiently inventory is generated and sold.

- Each department tracks its conversion costs in order to determine the quantity and cost per unit (see TBD; we discuss this concept in more detail later).

- Prime cost calculation is important to determine the actual input costs involved in manufacturing.

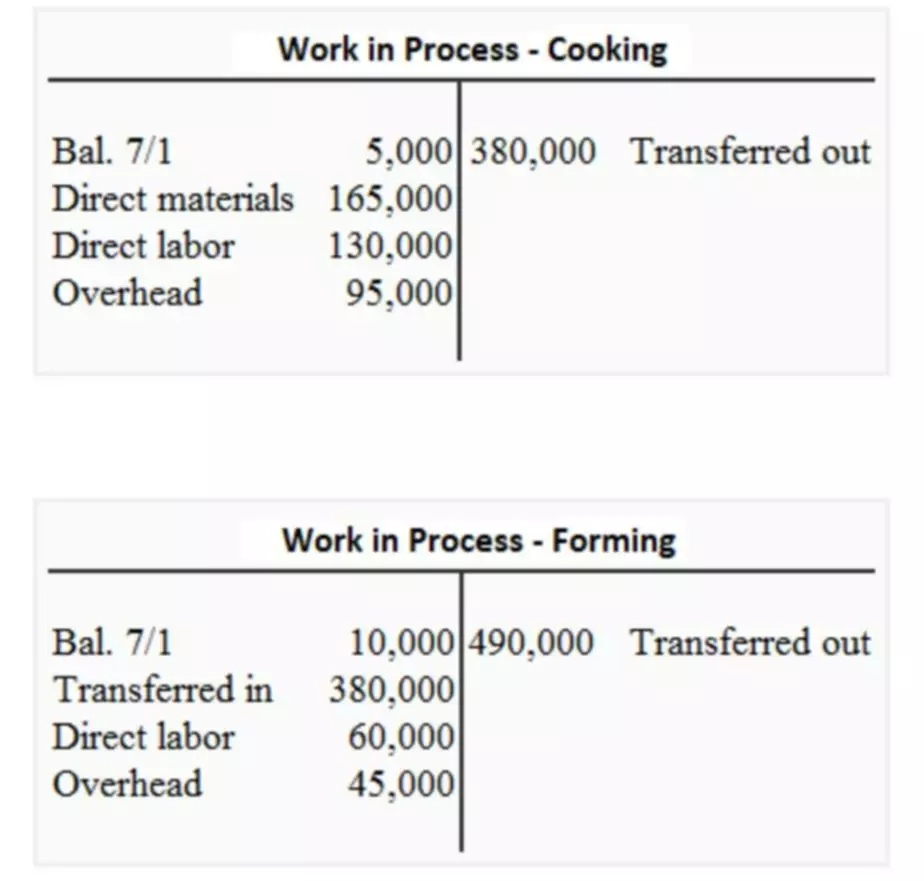

Therefore, once the batch of sticks gets to the second process—the packaging department—it already has costs attached to it. In other words, the packaging department receives both the drumsticks and their related costs from the shaping department. For the basic size 5A stick, the packaging department adds material at the beginning of the process. The 5A uses only packaging sleeves as its direct material, while other types may also include nylon, felt, and/or the ingredients for the proprietary handgrip. Direct labor and manufacturing overhead are used to test, weigh, and sound-match the drumsticks into pairs.

Dictionary Entries Near conversion cost

One can arrive at total period costs by closely monitoring and reporting the expenses that aren’t related to manufacturing a product. Bruce’s Bike Company is a bicycle manufacturer that specializes in high-end 10-speed bikes. Bruce is trying to figure out what his conversion costs are for the quarter in order to estimate his finished inventory for theinterim financial statements. It is used commonly in manufacturing units like paper, steel, soaps, medicines, vegetable oils, paints, rubber, and chemicals. The term conversion costs often appears in the calculation of the cost of an equivalent unit in a process costing system. If they were 100% complete with regard to conversion costs, then they would have been transferred to the next department.

For example, the raw materials for bread, which are typically eggs, flour, and yeast, don’t convert into bread on their own. As time passes, there will be more ways to gauge your campaign’s performance. And the best you can do is stay updated and make great use of these metrics.

For service organizations, cost of goods sold may be referred to as Cost of Services. This typically includes the cost of direct labor and manufacturing overhead (e.g. https://www.bookstime.com/ indirect materials, utility costs, depreciation, etc.). Some units might be partially complete during the manufacturing process, and others might be complete.

- Mostly, coversion costs represents the costs of all such activities or resources that have been applied in converting raw materials to finished items.

- Therefore, once the batch of sticks gets to the second process—the packaging department—it already has costs attached to it.

- Direct labor costs are the wages paid to the employees engaged in manufacturing a product or provision of service.

- And keep these numbers in mind while getting rid of a keyword.

It is based on the accounting equation that states that the sum of the total liabilities and the owner’s capital equals the total assets of the company. Means the expenses directly attributed to each unit of product or the process. These include electricity bills, rent, depreciation, plant insurance, repairs and maintenance of plants, etc.

What does the term conversion costs mean?

And it will increase your conversion rate and reduce the conversion cost. Every metric gives you a report card of your marketing campaign. Eventually, it means that every conversion out of this campaign costs you $50!

2022 Year-End Tax Planning Strategies for Individuals – Marcum LLP

2022 Year-End Tax Planning Strategies for Individuals.

Posted: Tue, 29 Nov 2022 14:30:00 GMT [source]